Choosing a DAO Wrapper: some thoughts for Radix

Introduction

Radix is currently considering where and how to structure its new DAO wrapper entity. This document is designed to be an aid to the internal discussions of Radix. It arises from observations of the ongoing discussion within Radix about how to restructure itself. It is presented by DAO SPV, which specializes in providing legal entities for DAOs and other web3 projects.

Discussions within Radix have mentioned Cayman and Panama foundations, DUNAs, MIDAO LLCs, and ADGM DLT Foundations. We will therefore have a look at these , as well as make some wider points about DAO wrappers

TLDR: Foundations are the dominant DAO wrapper form, but don’t fully wrap the DAO token holders themselves. If full wrapping is preferred by Radix, then DUNA, MIDAO LLC, ADGM, and the Swiss Association are the main options. DUNA however is unlikely to be a good choice - it is untested, and pulls DAOs into the US regulatory umbrella.

DAOs - the main costs

There are 6 primary cost avenues in setting up a DAO wrapper. When considering the relative costs of a DAO wrapper, it is important to remember that these different workstreams mean that the overall cost of the DAO is always higher than the initial setup fee.

- Entity formation & ongoing admin fees: entity setup, registered office fees, government fees, etc. These are a mix of one-off and annual fees.

- Director / manager fees: these vary with the jurisdiction and the extent to which a director is providing hands-on control. Where directors / managers are used, these will require annual fees.

- Legal fees: to the extent that the DAO wants to have external advice for writing up DAO constitutions, byelaws, and intern entry agreements, they will rely on a lawyer. These fees tend to be one-off fees.

- DAO ops: Many DAOs want to subcontract elements of their governance and treasury management. In this case, they hire external service providers

- Accounting fees: accounting, bookkeeping etc as required

- Tax advisory fees: ensuring that the DAO and DAO tokenholders is not exposed to any unexpected tax risk

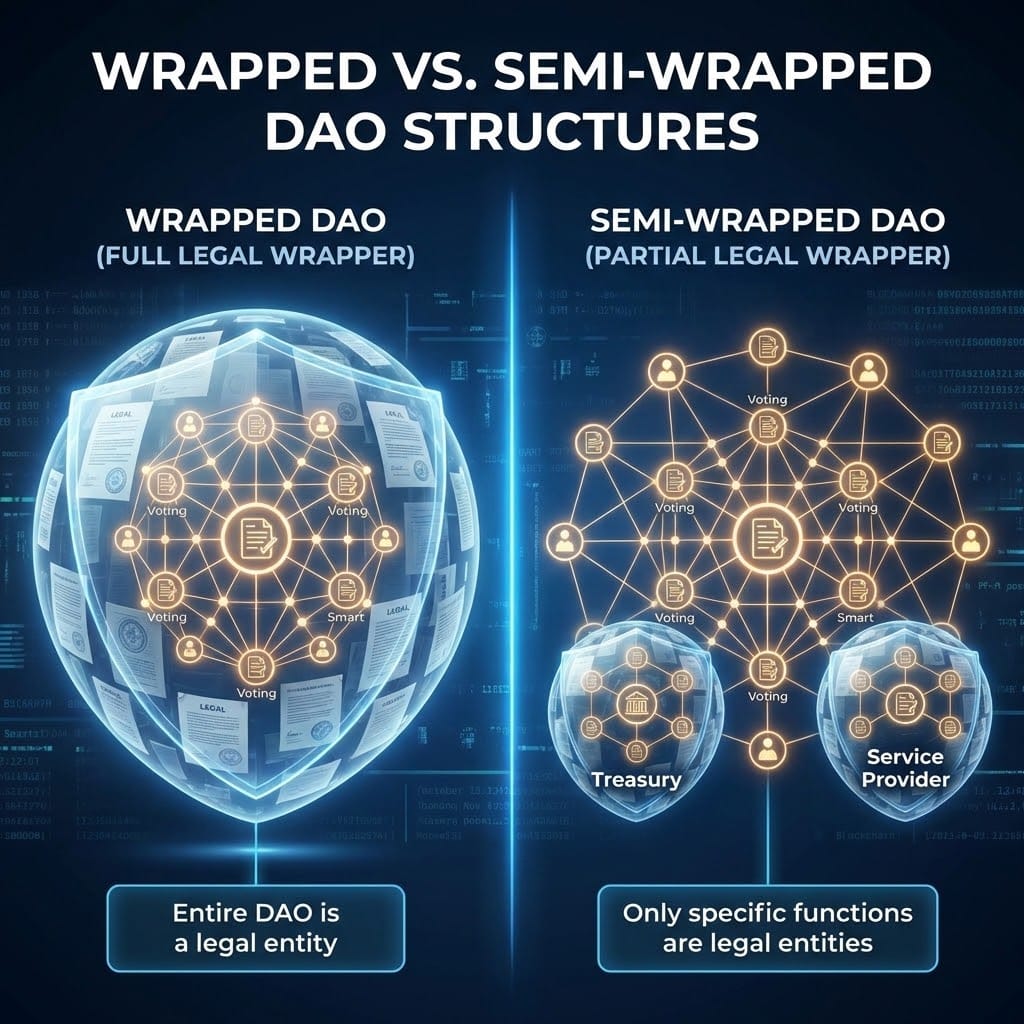

Wrapped and semi-wrapped DAOs

The primary dividing line among DAO wrappers is between fully wrapped and semi wrapped entities. The dominant form of DAO wrapper is the foundation, especially those in Cayman and Panama. The use of foundations for DAOs represents an innovative re-purposing of pre-existing legal structures to suit web3 needs. However, there are a number of DAO and web3 specialised structures that were designed with web3 in mind. From this difference arises wrapped vs semi wrapped DAOs.

In each case, an entity exists to provide legal personality for the project, and limited liability for the project and its actions.. However, how this happens varies:

- Fully-wrapped DAO: In this case, individual members of the DAO are members of the DAO wrapper entity itself. Through owning governance tokens, they are members of the entity and have rights within the entity; this will include things like the right to vote on proposals, change or remove managers etc. Examples include the Swiss Association, MIDAO LLC, and ADGM DLT Foundation.

- Semi-wrapped DAO:. Here, the entity has been set up to advance the needs of the project and to execute the will of the DAO. However, the on-chain DAO is formally distinct from ‘the DAO’ itself. Instead, the on-chain DAO provides instructions to the wrapper entity and the human directors that run it. Examples include the Cayman and Panama foundations.

What questions should we be asking?

- Do we want to rely on humans for (a) execution and (b) governance? Foundations need more human involvement. They don’t allow automated governance (except the DLT foundation to some extent), and you cant automate their inner operations with smart contracts. Being very decentralised and on-chain has its uses but comes at a cost. If you tell a bank, for instance, that your DAO has no directors/ managers / administrators, thy are much less likely to give you a bank account.

- How much disclosure do we want? Different DAO options have different disclosure requirements

- Who does the DAO need to deal with? Funders, banks, real-world entities will be more used to dealing with foundations and will have a preference for jurisdictions they see as reputable. This usually means working through tried and tested wrappers. However, if the DAO doesn't need to deal with these, it is less of an issue.

- How much do we care about tax? Some DAO wrappers require a limited amount of tax to be paid.

- Who do we want to carry out things for the DAO? Who will do work for the DAO, and where will they be? Depending on how arms length they are this can have tax implications

- Do we / will we have an opco, and where will this be based? The relationship of the opco to the DAO can have an impact on how decentralised it appears to regulators and tax authorities

- Where are the bulk of our token holders based? This impacts on the extent to which token holders will want to be pulled into certain jurisdictions through choice of DAO wrapper

The wrapper entities

DUNA

What it is: Decentralized Unincorporated Nonprofit Association, a special entity type in Wyoming USA. This is a fully-wrapped DAO; token holders are members of the entity. The DUNA law allows smart contracts to be used in the governance of the entity

Roles & requirements:

- Members: The token holders. The DUNA must have at least 100 members.

- Administrators: Individuals which the DUNA delegates specific tasks. These individuals are optional;

- Operating agreement: needs an operating agreement to law out how the entity will function

Costs: $1,000; does not include administrators, ancillary costs

Banking: Available , but harder if you don’t have administrators for the bank to deal with

Pros:

- Wrapper: Provides legal personality, limited liability etc.

- Tax flexibility: Can be taxed either as a corporation or a non-profit.

- On-chain operations: Enables on-chain governance & operations.

Cons:

- The USA: Use of a DUNA brings the project into the regulatory ambit of the USA. For projects without a US nexus, this is inadvisable, and imposes significant US related risks and costs. Notably, federal regulators will have primacy over Wyoming.

- Untested: this remains a comparatively new eneitty type

- Non-profit: the DUNA does not allow distribution of profits to token holders

A general reflection: These have not really taken off as of yet. As few as 3 existed in December. International web3 lawyers strongly advise against them for projects that are not seeking a strong US nexus. DUNAs have been heavily promoted in the US market but have a limited rationale outside.

MIDAO LLC

What it is: Marshall Islands DAO LLC. A very flexible DAO wrapping option. Like the DUNA, this can be a fully-wrapped DAO; token holders can be members of the entity. It also allows for a high degree of automation; MIDAO law allows smart contracts to be used in the governance of the entity

Roles and requirements:

- Members: Token holders can be admitted as members

- Managers: These are individuals and entities appointed to handle operations. Members can be a single person, a multisig wallet, or even another DAO.

- Operating Agreement: Central corporate constitution, optionally linked to on-chain governance.

- Smart Contracts: Not people, but they can be named in the documents as governance engines.

Costs: $9500 in setup fees; $5000 annual (not including manager, officers)

Banking: Available , but harder if you don’t have manager for the bank to deal with

Pros:

- Wraps the DAO.

- The potential lack of human directors is a positive for some projects (though a negative for many others).

- Flexible.

- Easy token launch in Marshall Islands

Cons

- Tax: for profit MIDAO LLCs have a 3% tax

- Jurisdiction reputation: Marshall Islands is relatively unknown, many counterparties wont like it

ADGM DLT Foundation

What it is: Abu Dhabi Global Markets DLT Foundation. A UAE based entity. This purpose built entity enables ‘fully wrapped’ DAOs. The DLT Foundations Regulations 2023 that allows DAOs and Web3 entities to establish a foundation entity recognising on-chain governance and token issuance.

Roles and requirements:

- Founder: either individuals or a company

- Council members: Needs a council, this must have 2-16 members

- Beneficiaries: Needs beneficiaries. If the foundation issues tokens, it can be the beneficiaries

- Foundation charter: forms the DAO constitution. This can be used to maximise the power of the token holders, or of the council

Costs: $14000 + in setup and licensing fees; $25,000 required initial asset value. Annual; $8000 for license, $4,000 + for registered services etc

Pros: It is a web3 specialised entity type. Fully wraps the DAO. Is geopolitically neutral.

Banking: Available

Cons:

- 9% tax, though this can be reduced to 0% on qualifying income

- High disclosure requirements - mandatory audits, for instance

- Will take longer to set up

- Comparatively untested. Only 9 set up by q2 2025

Panama

What it is: The Panama Private Interest Foundation. It is a well known and popular DAO wrapper tool. It is functionally similar to the Cayman foundation

Roles and requirement:

- Foundation council: Provides day to day management. Act according to Foundation constitution + their fiduciary responsibilities

- Protectors: ensure Counsellors work towards Foundation aims. May remove Councillors

Costs: Setup costs $5,000; annual costs, $2,500+

Banking: Available, though not all banks will deal with Panama

Pros:

- Speed and costs: Cheap & speedy to set up

- Well-known: Panama is a well known jurisdiction, and foundation is a well known and well understood entity

- Reporting: there is no audit requirement

- Tax: 0% tax rate

- Tokens: Panama is also a good token launch juridiction

Cons

- Non web3 native: it does not enable on-chain governance of the entity

- Panama: has a mixed reputation

Swiss Association

What it is: A Swiss entity type. In recent years it has become popular for DAOs and other web3 purposes, and has displaced the Swiss Foundation as a web structuring tool.

Roles and requirement:

- Constitution: formed via articles of association

- Members: requires at lead 2 members, who can be token holders

- Board: Responsible for the daily activities of the foundation. Must have at least 1 members

- Assembly: The voting collective of members. Appoints the board. Can amend the constitution.

Costs: Starts from $9,500+ ; Annual $7,200 +

Banking: Available, but expensive

Pros:

- Governance: The members / board / assembly distinction works well for many DAOs seeking to delegate powers.

- Jurisdiction: Switzerland has a high regulation

- Expertise: high web3 professional services expertise in Switzerland

- Privacy: if the association does not have commercial activity, it does not need to register

Cons

- Tax: 4.25

- Non web3 native: Does not enable direct smart contract governance. However, token holders can be deemed as members of the association and have voting rihtes

- Not for profit: while it can engage in commercial activities, it cannot be a for-profit entity.

FAQ

Do VCs hate foundations?

No. Foundations - Swiss, Cayman, and Panama foundations, with a long tail of entities in more niche places like Seychelles, St Kitts etc - are the dominant form of web3 wrapper. Certain self-interested US VCs proclaimed the ‘end of foundations’ and promoted local alternatives, but this does not reflect the reality of the market, founders, or what the legal industry tend to advise

Is a US nexus a good idea?

Good ideas and bad ideas are always relative to the needs of the project. Projects that are not significantly based in the USA should think carefully about moving themselves there by utilizing a US based wrapper entity. Despite some stated being po web3 , federal law still applies. It also pulls the project into US regulatory auspices.